Outsource Payroll in the Netherlands: A 2026 Employer’s Guide

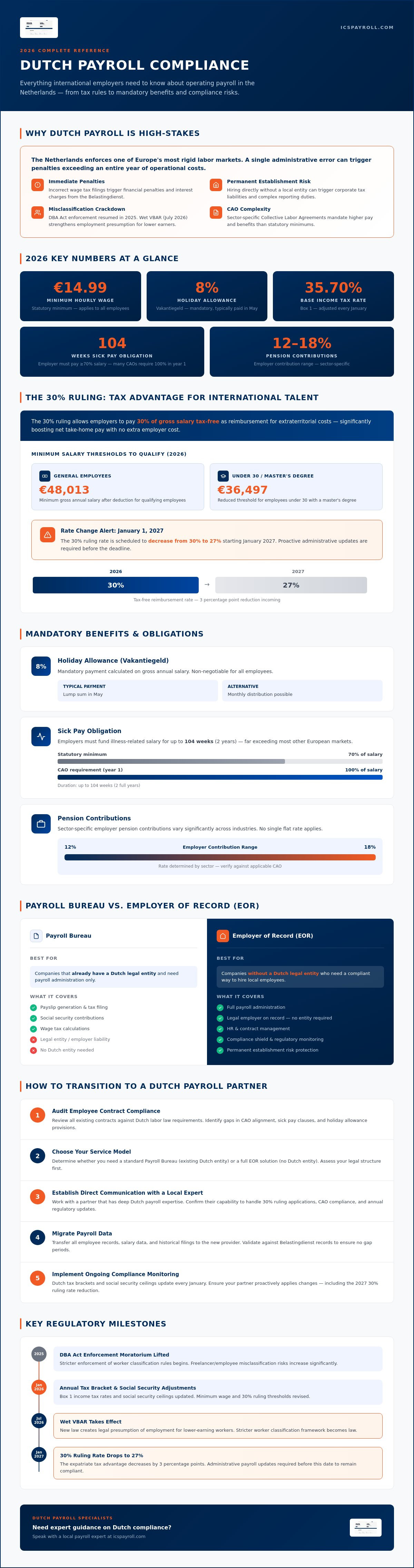

In the Netherlands, a single administrative oversight in your payroll filing can trigger penalties that far outweigh the cost of an entire year's operations. It's a high-stakes environment where the Dutch Tax Authority, the Belastingdienst, maintains an uncompromising stance on precision. If you've decided to outsource payroll Netherlands operations, you're likely looking for more than just a software solution; you need a compliance shield that protects your business from local legal risks.

We understand that managing the nuances of the 30% ruling or calculating the mandatory 8% holiday allowance feels like a significant burden. You want to focus on your international strategy, not deciphering the €14.99 statutory minimum hourly wage or complex sick pay obligations. This guide will help you master these Dutch payroll complexities and discover how to streamline your operations with a specialized local partner. We'll examine the 2026 regulatory landscape, providing a clear roadmap to full compliance, reduced overhead, and accurate payments for your team.

Key Takeaways

- Master the rigid requirements of Dutch labor laws, including social security contributions and sector-specific levies, to avoid costly Belastingdienst penalties.

- Understand how to correctly implement the 30% ruling tax advantage and calculate the mandatory 8% holiday allowance for the 2026 fiscal year.

- Determine whether a standard payroll bureau or a full Employer of Record (EOR) model is the most effective way to outsource payroll Netherlands operations for your business.

- Learn the essential steps for a seamless transition, from auditing employee contract compliance to establishing direct communication with a local expert partner.

Navigating the Complexity of Dutch Payroll Compliance

The Netherlands maintains one of the most sophisticated and rigid labor markets in Europe. For international employers, payroll represents a complex intersection of tax law, social security mandates, and sector-specific pension requirements. Successfully managing these variables requires deep local knowledge that goes beyond simple salary calculations. A broader understanding of the Dutch economic overview reveals a system designed to protect employees through extensive social safety nets, all funded by precise employer contributions. This environment leaves no room for error.

If you hire staff directly without a local legal entity or a dedicated partner, you face the risk of "Permanent Establishment." This status can lead to unexpected corporate tax liabilities and complex reporting duties. When businesses decide to outsource payroll Netherlands processes, they effectively build a defensive wall between their global strategy and local regulatory scrutiny. This approach provides a necessary buffer against the Belastingdienst (Dutch Tax Authority) and its stringent audit protocols.

The Risks of Local Non-Compliance

Incorrect wage tax filings lead to immediate financial penalties and interest charges. The Dutch authorities have increased their focus on employee misclassification following the 2025 lifting of the DBA Act enforcement moratorium. With the expected introduction of the Wet VBAR in July 2026, the legal presumption of employment for lower-earning workers becomes even stricter. Additionally, many sectors are governed by Collective Labor Agreements (CAO). These agreements often mandate higher pay scales and more generous benefits than statutory minimums, making compliance a moving target for those without local expertise.

Why In-House Management Often Fails for Foreign Firms

Foreign firms struggle because Dutch tax regulations change annually. For instance, Box 1 income tax brackets and social security ceilings are adjusted every January. Managing this in-house requires a specialist who understands the nuances of the 35.70% base tax rate and the phasing out of general tax credits. Language barriers also present a significant hurdle. Most government portals and legal documents are in Dutch. Hiring a dedicated local expert is often prohibitively expensive for companies with smaller teams, making specialized outsourcing the most logical path to operational security.

Key Features of the Dutch Payroll System: What to Expect

Operating a business in the Netherlands requires an understanding of specific financial obligations that differ significantly from other European markets. The Dutch system is built on a foundation of social security and mandatory employee benefits. When you outsource payroll Netherlands services, your provider must account for these variables with clinical precision to ensure both legality and employee satisfaction. Compliance is not just about avoiding fines; it's about maintaining the specialized standards outlined in Dutch payroll tax regulations.

The 30% Ruling: A Strategic Tax Advantage

The 30% ruling remains the most effective tool for attracting international talent to the Dutch market. It functions as a tax-free reimbursement for extraterritorial costs, requiring a minimum gross annual salary of €48,013 after the deduction for qualifying employees in 2026. For employees under the age of 30 with a master's degree, the qualifying threshold is €36,497. This incentive allows employers to provide 30% of an employee's gross salary tax-free, which significantly increases the net take-home pay without increasing the employer's total cost.

It's vital to plan for upcoming legislative shifts. While the 30% rate is applicable throughout 2026, it is scheduled to decrease to 27% starting January 1, 2027. Managing these transitions requires proactive administrative updates to remain compliant. If you are hiring international staff, our team can streamline the process by managing your 30% ruling application directly.

Statutory Benefits and Dutch Labor Standards

Beyond the base salary, several statutory benefits are non-negotiable. The 8% holiday allowance (Vakantiegeld) is a mandatory payment calculated on the employee's gross annual salary. It's typically paid as a lump sum in May, though some employers choose to distribute it monthly. Sick pay obligations are also notably extensive. Employers are legally required to pay at least 70% of an employee's salary for up to 104 weeks of illness. In practice, many Collective Labor Agreements (CAOs) mandate 100% payment during the first year.

Pension requirements add another layer of complexity. Contributions are often sector-specific, with employer contributions typically ranging from 12% to 18% of the salary. You must also consider mandatory insurance for occupational disability and unemployment. These costs are capped at a maximum social security base of €79,409 for the 2026 fiscal year. Ensuring these figures are calculated correctly is the primary reason businesses move away from in-house management toward specialized local experts.

Choosing Your Model: Payroll Service vs. Employer of Record (EOR)

Deciding how to outsource payroll Netherlands depends entirely on your current legal footprint. You must choose between a standard payroll administration service and a full Employer of Record (EOR) model. While both handle the mechanical aspects of salary distribution, they differ fundamentally in terms of legal liability and corporate structure requirements. This choice defines your relationship with the Dutch authorities and your speed of execution.

The EOR model serves as a comprehensive solution for companies without a Dutch legal entity. In this arrangement, the provider acts as the legal employer. They assume all risks related to labor law, social security, and tax compliance. This model is particularly effective for businesses testing the Dutch market or hiring a small team of remote experts. It eliminates the need for a local BV, saving months of administrative effort and significant incorporation costs.

The EOR Advantage for International Expansion

Speed to market is the defining benefit of the EOR model. You can onboard employees in a matter of days rather than waiting for the completion of corporate registration. The EOR manages the entire employee lifecycle, from drafting compliant contracts to handling mandatory insurance. They also ensure your operations meet the Waadi registration requirements for supplying personnel. This approach allows your HR team to focus on talent management while the local expert handles the bureaucratic execution and legal shielding.

Standard Payroll Administration for Established BVs

If you have already established a Dutch BV, you require a specialized payroll administration partner. This model focuses on the precise execution of monthly filings and tax statements. Your partner ensures that every Loonaangifte (wage tax declaration) is submitted by the last day of the following month. They also manage the complexities of sector-specific Collective Labor Agreements (CAOs), which often dictate specific pension contributions and overtime rates. This service integrates with your existing accounting software to provide a seamless flow of financial data and reporting.

The choice involves a strategic cost-benefit analysis. Establishing a local entity requires upfront investment in legal fees, tax advice, and ongoing corporate compliance. An EOR carries a service fee but removes these overheads entirely. For many international firms, the decision to outsource payroll Netherlands through an EOR is the preferred vehicle for Dutch market entry because it provides immediate protection against local labor risks and the ability to scale without corporate restructuring.

How to Transition to a Dutch Payroll Partner

Moving your administrative burden to a local expert is a strategic shift that requires clinical precision. It is not just about moving spreadsheets. You are aligning your business with the Belastingdienst's rigid reporting cycle. When you choose to outsource payroll Netherlands operations, the transition period is the most critical phase for long-term compliance. A structured approach ensures that no data is lost and no deadlines are missed.

The initial phase involves a comprehensive audit of current employee data and contract compliance. You must verify that every employment agreement aligns with Dutch labor standards and any applicable Collective Labor Agreements (CAO). This is the time to confirm the 30% ruling status for international staff and ensure personnel files are complete. Once the data is verified, you must establish a clear communication flow between your HR team and the local provider. This prevents delays when processing monthly changes such as sick leave, new hires, or bonus payments.

A successful transition relies on a fixed payroll calendar. This schedule must account for the Loonaangifte (wage tax declaration) deadline, which falls on the last day of the following month. Before the final go-live, execute a "shadow run." This is a parallel payroll execution where the new provider calculates a previous month's data to ensure their results match your historical records exactly. This step confirms that social security contributions and holiday allowance accruals are calculated with 100% accuracy.

Data Migration and GDPR Security Standards

Security is a non-negotiable priority during data migration. All sensitive employee information must be transferred via encrypted channels to meet EU and Dutch GDPR standards. Your provider must also demonstrate a robust system for record retention. Dutch law requires payroll records to be kept for 7 years. Accurate historical data is your primary defense during a retrospective tax audit.

Setting Up Monthly Filing and Payment Cycles

Coordinating the Loonheffingen (wage tax) cycle is the final step. Your partner will manage the flow of net salary payments to employees while ensuring the tax authority receives the correct amounts on time. This process also includes managing local travel allowances, such as the standard kilometer reimbursement, and expense claims. Transitioning to a local expert allows you to outsource payroll Netherlands management with confidence, knowing the mechanical execution is handled. Contact us today to start your transition to a compliant Dutch payroll model.

Strategic Payroll Management with ICSPayroll

Managing a Dutch workforce requires a level of specialized focus that generic global platforms often fail to provide. While automated systems handle basic calculations, they frequently lack the nuance required for the Belastingdienst's specific reporting demands. ICSPayroll provides the localized expertise necessary to act as the bridge between your international strategy and local execution. Our model prioritizes direct, human-led interaction, ensuring that your business receives precise advice based on current 2026 regulations rather than automated responses.

We act as a protective guardian for your Dutch operations. Our team manages the entire payroll lifecycle with clinical precision, from calculating the mandatory 8% holiday allowance to processing 30% ruling applications. By securing these specific tax advantages, we help you maximize employee retention and maintain a competitive edge in the local market. When you choose to outsource payroll Netherlands operations to a dedicated local expert, you eliminate the administrative friction that often stalls international growth.

Local Expertise for International Growth

ICSPayroll serves as your boots on the ground for Dutch compliance. We provide international CFOs with transparent reporting and clear process visibility, which is essential for financial planning. This transparency is vital when transitioning international teams to the Dutch market for the first time. We've successfully managed numerous transitions, ensuring that each employee is integrated into the system without delay. Our dedicated account managers provide the continuity and accountability that large, faceless outsourcing firms simply cannot match.

Streamlined Compliance for Remote Teams

Managing a distributed workforce in the Netherlands requires constant attention to shifting labor standards. Every contract must align with the 2026 statutory requirements, including the July 1 minimum wage increase to €14.99 per hour. ICSPayroll ensures your remote staff are paid accurately and on time, regardless of where they're located. We handle the technical integration of local travel allowances and expense reimbursements, ensuring every payment is compliant with Dutch tax law.

Maintaining a secure and compliant presence in the Netherlands doesn't have to be an administrative burden. Our specialized focus provides the reliability your business needs to thrive in a complex regulatory environment. Optimize your Dutch payroll with ICSPayroll today to secure your operational future and provide your employees with the peace of mind they deserve.

Secure Your Dutch Operational Future

Mastering Dutch payroll requires more than administrative diligence; it demands a proactive approach to evolving labor laws. Whether you are managing the mandatory 8% holiday allowance or navigating the specific 2026 salary thresholds for highly skilled migrants, accuracy is your primary defense against regulatory friction. By choosing to outsource payroll Netherlands operations, you secure a stabilized foundation for international growth while protecting your business from the complexities of the Belastingdienst.

ICSPayroll acts as your local expert and protective guardian in this high-stakes environment. Our team provides specialized EOR and payroll services designed to mitigate risk and remove administrative burdens. As 30% ruling application experts, we ensure your talent remains satisfied and your filings remain beyond reproach. We provide the human-led support that global, automated platforms simply cannot replicate.

Get a compliant Dutch payroll solution from ICSPayroll today. We look forward to helping you establish a seamless, professional presence in the Dutch market.

Frequently Asked Questions

What is the 30% ruling and how do we apply for it?

The 30% ruling is a tax incentive that allows employers to provide 30% of a qualifying employee’s gross salary as a tax-free allowance. For the 2026 fiscal year, the qualifying salary threshold is €48,013, or €36,497 for employees under 30 with a master's degree. Applications are submitted directly to the Belastingdienst, and our team manages the entire filing process to ensure all criteria are met.

Do I need a Dutch bank account to pay employees in the Netherlands?

You don't strictly need a Dutch bank account if you partner with a local provider that manages payments through their own SEPA-compliant infrastructure. While SEPA accounts from other EU countries are legally accepted, using a local partner simplifies the distribution of net salaries and tax payments. This approach ensures your business remains compliant without the administrative burden of opening a local legal entity.

What are the mandatory social security contributions for employers in 2026?

Employers must contribute to several funds, including the General Unemployment Fund (AWf) at 2.74% for permanent contracts and the Health Insurance Contribution (Zvw) at 6.10%. These contributions are capped at a maximum social security base of €79,409 for 2026. You must also account for the differentiated Aof premium, which is 6.27% for smaller employers, to maintain full regulatory compliance.

How does sick pay work for outsourced payroll in the Netherlands?

Dutch law requires employers to pay at least 70% of an employee’s salary for up to 104 weeks during illness. In many industries, Collective Labor Agreements (CAO) mandate 100% payment during the first year. When you choose to outsource payroll Netherlands operations, your provider manages the necessary reporting to the occupational health service (Arbodienst) and ensures all payments align with these statutory requirements.

Can I hire a Dutch employee through an EOR if I do not have a Dutch entity?

Yes, hiring through an Employer of Record (EOR) is the most efficient way to employ staff in the Netherlands without establishing a local legal entity. The EOR acts as the legal employer, assuming all risks and administrative duties associated with Dutch labor law. This model allows you to outsource payroll Netherlands management entirely while maintaining a compliant and professional presence in the market.

What is the 13th-month salary and is it mandatory in the Netherlands?

The 13th-month salary is not a statutory requirement in the Netherlands. It is a discretionary benefit often included in individual employment contracts or specific Collective Labor Agreements (CAO). When applicable, it is typically equivalent to one month's gross salary and is paid in December. Employers use this benefit as a strategic tool for talent retention and competitive compensation packages.

How long does it take to set up payroll for a new hire in the Netherlands?

Onboarding a new hire typically takes between 1 to 3 business days once the underlying payroll infrastructure is established. If you are setting up an EOR arrangement for the first time, the initial implementation usually takes 1 to 2 weeks. This timeline includes drafting compliant contracts, verifying employee data, and ensuring all tax registrations are active with the Dutch authorities.

What are the penalties for non-compliant payroll in the Netherlands?

Non-compliance results in immediate financial penalties, including fines for late Loonaangifte filings and interest charges on unpaid wage taxes. The Belastingdienst also conducts audits for "bogus self-employment" following the 2025 lifting of the DBA Act enforcement moratorium. Incorrectly classifying workers can lead to retrospective social security claims and significant legal costs, making local expertise a vital safeguard for your business.

Frequently Asked Questions

The 30% ruling is a tax incentive that allows employers to provide 30% of a qualifying employee’s gross salary as a tax-free allowance. For the 2026 fiscal year, the qualifying salary threshold is €48,013, or €36,497 for employees under 30 with a master's degree. Applications are submitted directly to the Belastingdienst, and our team manages the entire filing process to ensure all criteria are met.

You don't strictly need a Dutch bank account if you partner with a local provider that manages payments through their own SEPA-compliant infrastructure. While SEPA accounts from other EU countries are legally accepted, using a local partner simplifies the distribution of net salaries and tax payments. This approach ensures your business remains compliant without the administrative burden of opening a local legal entity.

Employers must contribute to several funds, including the General Unemployment Fund (AWf) at 2.74% for permanent contracts and the Health Insurance Contribution (Zvw) at 6.10%. These contributions are capped at a maximum social security base of €79,409 for 2026. You must also account for the differentiated Aof premium, which is 6.27% for smaller employers, to maintain full regulatory compliance.

Dutch law requires employers to pay at least 70% of an employee’s salary for up to 104 weeks during illness. In many industries, Collective Labor Agreements (CAO) mandate 100% payment during the first year. When you choose to outsource payroll Netherlands operations, your provider manages the necessary reporting to the occupational health service (Arbodienst) and ensures all payments align with these statutory requirements.

Yes, hiring through an Employer of Record (EOR) is the most efficient way to employ staff in the Netherlands without establishing a local legal entity. The EOR acts as the legal employer, assuming all risks and administrative duties associated with Dutch labor law. This model allows you to outsource payroll Netherlands management entirely while maintaining a compliant and professional presence in the market.

The 13th-month salary is not a statutory requirement in the Netherlands. It is a discretionary benefit often included in individual employment contracts or specific Collective Labor Agreements (CAO). When applicable, it is typically equivalent to one month's gross salary and is paid in December. Employers use this benefit as a strategic tool for talent retention and competitive compensation packages.

Onboarding a new hire typically takes between 1 to 3 business days once the underlying payroll infrastructure is established. If you are setting up an EOR arrangement for the first time, the initial implementation usually takes 1 to 2 weeks. This timeline includes drafting compliant contracts, verifying employee data, and ensuring all tax registrations are active with the Dutch authorities.

Non-compliance results in immediate financial penalties, including fines for late Loonaangifte filings and interest charges on unpaid wage taxes. The Belastingdienst also conducts audits for "bogus self-employment" following the 2025 lifting of the DBA Act enforcement moratorium. Incorrectly classifying workers can lead to retrospective social security claims and significant legal costs, making local expertise a vital safeguard for your business.