Employment Law in the Netherlands for Foreign Employers: 2026 Compliance Guide

The Netherlands maintains one of the most pro-employee legal frameworks in the world. A single oversight in a labor contract can lead to years of unintended financial liability. For international companies, the primary challenge isn't just finding talent; it's managing the complex landscape of employment law Netherlands for foreign employers without triggering a permanent establishment tax risk. You're likely concerned about the 104-week sick pay obligation or the strict dismissal laws that make operational flexibility feel out of reach.

We understand that these administrative burdens can overshadow your expansion goals. This 2026 compliance guide provides the professional clarity you need to hire securely and cost-effectively. You'll learn how to leverage the 30% ruling to attract top-tier talent while maintaining total regulatory alignment. We'll break down the mandatory 8% holiday allowance, the current €48,013 salary thresholds, and the strategic benefits of hiring through an Employer of Record to bypass the need for local entity incorporation.

Key Takeaways

- Understand the Polder Model's influence on Dutch employment relations to manage a landscape built on consensus and employee protection.

- Learn to accurately calculate mandatory costs, including the 8% holiday allowance and the financial commitment required for the two-year sick pay rule.

- Identify eligibility for the 30% ruling so it's easier to attract specialized international talent with tax-efficient compensation packages.

- Mitigate permanent establishment risks and bypass entity incorporation by leveraging employment law Netherlands for foreign employers through an Employer of Record.

- Prepare for 2026 legislative changes, such as the WTTA permit system and non-compete reforms, to ensure your hiring process remains fully compliant.

Understanding the Dutch Labor Market: A Pro-Employee Landscape

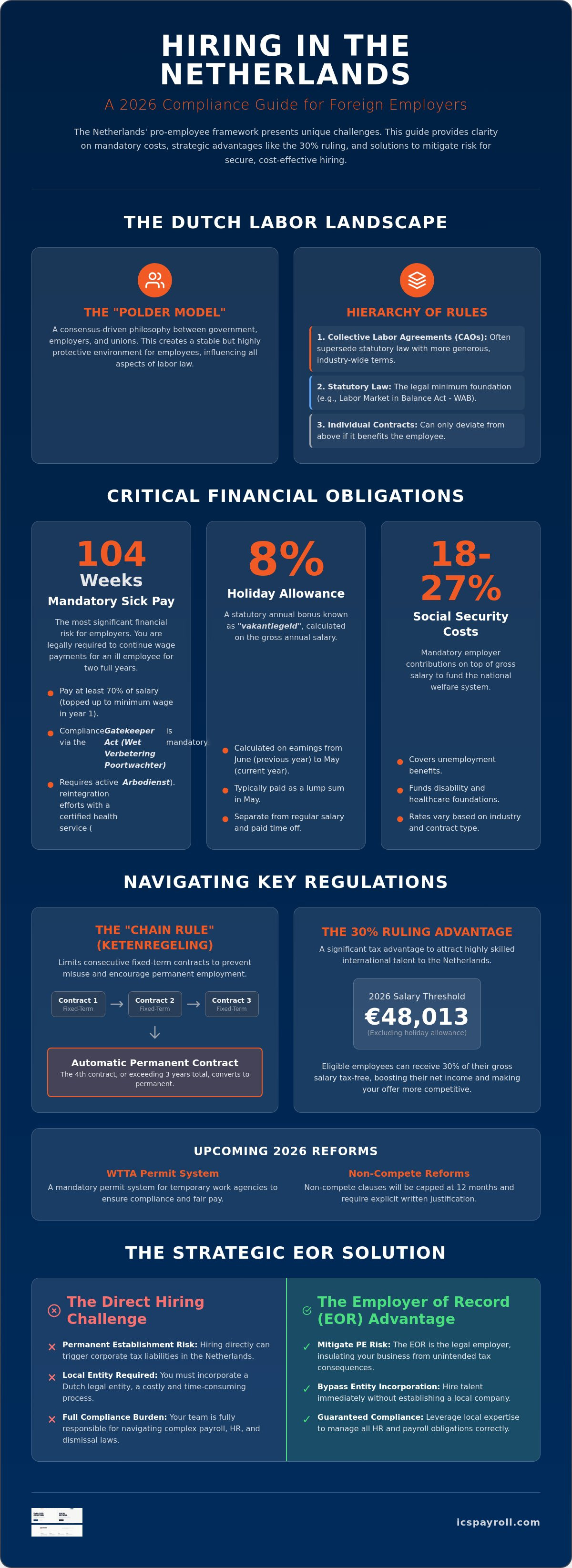

The Dutch labor market operates on the "Polder Model," a philosophy centered on consensus between the government, employers, and labor unions. While this approach ensures long-term industrial stability, it creates a regulatory environment that is significantly more protective of workers than many foreign jurisdictions. Mastering employment law Netherlands for foreign employers means accepting that the legal system is designed to safeguard the employee's position. This protectionist stance is reflected in everything from stringent dismissal procedures to the mandatory 104-week sick pay obligation.

In 2026, the landscape continues to evolve with the implementation of the Dutch Temporary Employment Reform (WTTA). This reform introduces a mandatory permit system for agencies and equal-pay obligations for temporary workers. Foreign entities must recognize that compliance isn't a one-time setup but an ongoing operational requirement in this sophisticated market. Adhering to these standards is essential to avoid the heavy fines associated with non-compliance.

The Hierarchy of Dutch Employment Rules

Dutch employment regulations follow a strict hierarchy. Statutory law provides the foundational rights, but these are frequently superseded by Collective Labor Agreements (CAOs). These agreements are negotiated at an industry or company level and often contain more generous benefits than the legal minimums. If a CAO is declared "universally binding" for your sector, you must follow its terms even if you weren't a party to the negotiations. Individual employment contracts sit at the bottom of this hierarchy; they can only deviate from the CAO or statutory law if the change benefits the employee. The Labor Market in Balance Act (WAB) serves as the primary legislative framework that makes flexible labor more expensive and regulated to encourage the use of permanent employment contracts.

Common Surprises for Foreign HR Managers

International HR teams often encounter friction with the "Chain Rule," known locally as the Ketenregeling. This rule permits a maximum of three consecutive fixed-term contracts within a three-year period. Once this limit is reached, the contract automatically converts into a permanent arrangement. Another mandatory requirement is the 8% holiday allowance. This is a statutory payment, typically disbursed in May, calculated based on the employee's gross annual salary. Standard working hours generally total 36 to 40 hours per week. While an "overtime culture" exists in some sectors, it's often compensated with time-off-in-lieu rather than simple cash payments. By 2026, foreign employers must also account for proposed non-compete clause reforms that cap restrictions at twelve months and require explicit written justification for every contract.

Mandatory Benefits and the Two-Year Sick Pay Obligation

In the Netherlands, compensation goes beyond the monthly base salary. The most prominent addition is the mandatory 8% holiday allowance (vakantiegeld). Employers calculate this by taking the total gross salary earned between June of the previous year and May of the current year. It's typically paid out as a lump sum in May. While some high-income contracts allow for this to be "all-in," most standard agreements require it as a separate line item. Beyond salary, employers contribute approximately 18% to 27% in social security premiums, covering unemployment, disability, and healthcare foundations.

The most significant financial risk within employment law Netherlands for foreign employers is the two-year sick pay obligation. If an employee falls ill, you're legally required to pay at least 70% of their salary for 104 weeks. If that 70% falls below the statutory minimum wage, you must top it up to the minimum level during the first year. Many Dutch employers choose to pay 100% in the first year to remain competitive. This obligation remains even if the illness is unrelated to work, making specialized "sick-pay insurance" a critical tool for risk mitigation.

Managing Long-Term Illness Compliance

Compliance during illness is governed by the Wet Verbetering Poortwachter (Gatekeeper Act). This legislation requires a proactive approach to reintegration. You must partner with a certified Arbodienst (Occupational Health Service) to monitor the employee's progress. The process follows a strict timeline: a problem analysis at week six, an action plan at week eight, and periodic evaluations. If the employee can't return to their original role, you must seek "internal placement" in a different position. If that's impossible, "external placement" with another employer becomes mandatory. Failure to document these steps can result in the UWV imposing a third year of mandatory wage payments. Utilizing a Dutch payroll administration partner ensures these administrative milestones are managed accurately.

Statutory Leave Entitlements in 2026

The statutory minimum for paid vacation is four times the number of weekly working hours. For a full-time employee, this is 20 days per year. However, the Dutch market standard is 25 days. Beyond vacation, the Netherlands has expanded its parental leave policies. Parents are entitled to nine weeks of partially paid leave during the child's first year, with the UWV compensating 70% of the daily wage up to the statutory cap. Partners also receive one week of fully paid leave and five weeks of additional leave at 70% pay. Employers must also account for emergency leave and short-term care leave, which provide necessary flexibility for employees facing urgent family matters.

The 30% Ruling: A Strategic Advantage for Foreign Employers

The 30% ruling remains the most effective recruitment tool within employment law Netherlands for foreign employers. This tax facility allows you to provide a tax-free allowance of up to 30% of an employee's gross salary to cover extraterritorial costs. For specialized roles, particularly in technology and engineering, this incentive often bridges the gap between a standard Dutch salary and the expectations of global talent. In 2026, the ruling provides a stable 30% rate for eligible employees, though it's vital to note that for rulings starting after January 1, 2024, this rate will decrease to 27% beginning in 2027.

Eligibility depends on the "150km rule." To qualify, the employee must have lived more than 150 kilometers from the Dutch border for at least 16 out of the 24 months preceding their first day of work. This rule effectively excludes residents of Belgium and large portions of Germany and Luxembourg. Beyond geography, the employee must possess specific expertise that is scarce in the Dutch labor market. While the Belastingdienst (Dutch Tax Office) generally assumes scarcity if the salary thresholds are met, the employer must still submit a formal joint application to secure the benefit.

Securing this ruling isn't automatic; it requires meticulous administrative execution. The employer is responsible for initiating the application within four months of the employee's start date to ensure full retroactivity. If the application is filed late, the ruling only applies from the first day of the month following the application month. This delay can result in thousands of Euros in lost tax benefits for the employee, potentially damaging the employment relationship before it has fully matured.

Salary Requirements for 2026

To qualify for the 30% ruling in 2026, the employee's taxable salary must meet specific annual thresholds. For most professionals, the minimum taxable salary is €48,013. A reduced threshold of €36,497 applies to employees under the age of 30 who hold a qualifying Master's degree. These figures are the taxable amounts after the 30% deduction has been applied. Employees granted this ruling can opt for partial non-resident taxpayer status; this allows them to be treated as non-residents for tax purposes regarding their savings and investments in Box 2 and Box 3, even while living in the Netherlands.

Administrative Execution of the Ruling

Once approved, the ruling must be processed through the monthly payroll as a tax-free reimbursement. This impacts more than just the net take-home pay. Since the taxable base is lower, social security contributions and pension accrual are also calculated on the reduced amount. This can lead to lower future benefits, a detail that must be clearly communicated to the employee during the onboarding phase. Managing these nuances for remote or hybrid teams requires precision to ensure the "work performed" aligns with Dutch tax jurisdiction. ICSPayroll handles the entire 30% ruling application process, from initial eligibility screening to the final submission to the Tax Office, ensuring your international hires receive their benefits without administrative delays.

Dismissal Law and Permanent Establishment Risks

Dutch labor law operates on the principle of "preventive dismissal testing." Unlike at-will jurisdictions, an employer cannot unilaterally terminate a contract without a valid legal ground and prior approval from a government body. This is a fundamental pillar of employment law Netherlands for foreign employers. Depending on the reason for dismissal, you must either apply to the Employee Insurance Agency (UWV) for economic redundancies or petition the District Court for performance or behavioral issues. Termination without these approvals is generally considered void unless the employee agrees in writing.

Every employee is entitled to a statutory severance, known as the transition payment (Transitievergoeding), from their first day of employment. In 2026, this payment is capped at €102,000 or one year's gross salary if that amount is higher. This obligation applies even if the employee is dismissed during their probationary period or if a fixed-term contract is not renewed. Understanding these exit costs is essential for accurate financial forecasting when building a Dutch team.

Compliant Termination Procedures

To avoid lengthy court battles or UWV applications, most employers opt for a Settlement Agreement (VSO). This allows for termination by mutual consent, where the employee waives their right to contest the dismissal in exchange for a negotiated severance and a notice period. If you choose to dismiss based on underperformance, you must provide a comprehensive "dossier" proving that you offered the employee a fair chance to improve through a formal Performance Improvement Plan (PIP). For redundancies, the "Reflective Test" (afspiegelingsbeginsel) must be applied to ensure the selection process follows a strict age-based and seniority-based logic rather than personal preference.

Mitigating Corporate Tax and Legal Risks

A frequent oversight for remote-first companies is the "Permanent Establishment" (PE) risk. Hiring a Dutch employee who performs core business activities or holds the authority to sign contracts can inadvertently create a local tax nexus. This triggers Dutch corporate tax obligations on a portion of your company's global profits. Additionally, the "Right to Work" check is a mandatory administrative step that cannot be delegated lightly. Failing to verify a non-EU employee's work permit can result in fines exceeding €8,000 per violation. Utilizing a local Employer of Record (EOR) acts as a legal firewall. The EOR becomes the official employer on paper, which effectively neutralizes PE risks while ensuring all local labor permits and "Right to Work" checks are strictly verified and maintained.

Hiring Without an Entity: The Employer of Record Solution

Establishing a local entity, such as a Dutch BV, is the traditional path for international expansion, but it's often inefficient for companies hiring a small or remote team. The administrative overhead of a BV involves notary fees, Chamber of Commerce registration, and the requirement for a local director. An Employer of Record (EOR) provides a faster, more flexible alternative. It allows you to delegate the legal complexities of employment law Netherlands for foreign employers to a local specialist while you maintain direct management of your team's daily activities. This model transforms a complex legal hurdle into a simple monthly service.

The EOR assumes all statutory responsibilities on your behalf. This includes calculating and filing payroll taxes, managing social security contributions, and securing mandatory insurances. The onboarding process is streamlined to ensure zero downtime. Once a service agreement is signed, the EOR issues a Dutch-compliant employment contract to the worker. Within days, the employee is registered with the tax authorities and ready to start. This eliminates the need for the foreign company to open a Dutch bank account or navigate the local tax system independently, providing immediate peace of mind.

The Operational Benefits of Local EOR

Speed is the most significant advantage of the EOR model. While entity incorporation can take months, an EOR allows you to hire in the Netherlands in less than a week. You avoid the high costs of local legal counsel and the ongoing burden of Dutch corporate tax filings. Because the EOR is the official employer, they handle the "Right to Work" checks and wage tax filings with 100% precision. This setup provides a secure bridge for foreign entities to enter the market without immediate long-term capital commitments or the risk of permanent establishment.

Why ICSPayroll is Your Compliance Partner

Many global EOR providers treat the Netherlands as just one of many regions in a vast portfolio. ICSPayroll maintains an exclusive focus on the Dutch market. This specialization ensures that our clients receive direct access to experts who understand the deep nuances of the 30% ruling and the complexities of the Gatekeeper Act. We pride ourselves on a human-centric approach; you'll speak with a dedicated professional rather than an automated ticketing system. Our transparent, no-nonsense communication style removes the guesswork from Dutch labor regulations and ensures your payroll is managed with clinical precision. Secure your Dutch compliance with ICSPayroll today.

Secure Your Dutch Expansion Strategy

Success in the Dutch market depends on more than just talent acquisition. It requires a precise understanding of the 104-week sick pay obligation and the strategic application of the 30% ruling. Navigating employment law Netherlands for foreign employers is a technical challenge that demands local expertise to avoid permanent establishment risks and administrative fines. By prioritizing compliance from day one, you transform these rigid regulations into a competitive advantage for your international team. You'll ensure long-term stability for your workers and financial security for your organization.

ICSPayroll serves as your dedicated bridge to the Dutch market. We remove the burden of local entity incorporation while providing expert oversight of payroll taxes and the 30% ruling application. Our human-led support ensures you have direct access to local experts who fully grasp the 2026 regulatory landscape. You can focus on scaling your operations while we handle the meticulous administrative details that keep your business protected. Schedule a compliance consultation with ICSPayroll to secure a risk-free hiring process for your Netherlands-based team. We're ready to help you build a stable and compliant presence in the Netherlands.

Frequently Asked Questions

Can I hire an employee in the Netherlands without a local legal entity?

You can hire employees in the Netherlands without incorporating a local entity by using an Employer of Record (EOR). The EOR acts as the legal employer, managing all payroll, tax, and social security obligations on your behalf. This allows foreign companies to enter the market quickly while remaining fully compliant with employment law Netherlands for foreign employers. It's the most efficient way to secure talent without the administrative burden of setting up a Dutch BV.

What is the mandatory holiday allowance in the Netherlands?

The mandatory holiday allowance is 8% of the employee's gross annual salary. This is a statutory requirement for all employees in the Netherlands and is typically paid as a lump sum in May. It's calculated based on the base salary plus any overtime or bonuses earned during the previous year. Employers must ensure this is clearly stated in the employment contract to avoid disputes during the annual payout period.

How much does it cost to employ someone in the Netherlands?

Beyond the gross salary, you should budget for employer social security contributions, which typically add 18% to 27% to the total employment cost. This percentage varies depending on the specific sector and the type of contract. You must also factor in the mandatory 8% holiday allowance and any secondary benefits such as pension contributions or travel allowances. These costs cover essential insurance for unemployment, disability, and healthcare foundations.

What is the 30% ruling and how do I apply for it?

The 30% ruling is a tax incentive for highly skilled migrants that allows you to provide a 30% tax-free allowance on their gross salary. To apply, both the employer and employee must submit a joint application to the Dutch Tax Office (Belastingdienst) within four months of the start date. In 2026, the minimum taxable salary threshold is €48,013 for most professionals, or €36,497 for those under 30 with a qualifying Master's degree.

How long is the probationary period in a Dutch employment contract?

The maximum probationary period is two months for an indefinite contract and one month for fixed-term contracts longer than six months but shorter than two years. Contracts with a duration of six months or less cannot legally include a probationary period. During this window, either party can terminate the employment relationship immediately without providing a specific reason or observing a notice period. It's a critical phase for assessing the fit between the employee and the organization.

What happens if my Dutch employee falls ill for a long period?

If an employee falls ill, you're legally required to pay at least 70% of their salary for up to 104 weeks. During the first year of illness, this payment must not fall below the statutory minimum wage. You must also follow the Gatekeeper Improvement Act, which mandates a strict reintegration process in partnership with an occupational health service (Arbodienst). Failure to document these reintegration efforts can lead to the UWV imposing a third year of mandatory wage payments.

Is it difficult to terminate an employment contract in the Netherlands?

Terminating a contract is more complex in the Netherlands because at-will employment doesn't exist. You generally need a valid legal ground and permission from either the UWV or a District Court, unless the employee agrees to a Settlement Agreement (VSO). Most employers choose the VSO route to avoid lengthy legal proceedings. This agreement allows both parties to part ways on mutually agreed terms, including the statutory transition payment and notice period.

What is the difference between an EOR and a payroll provider in the Netherlands?

An EOR acts as the legal employer of your staff, assuming all legal risks and compliance responsibilities under employment law Netherlands for foreign employers. A payroll provider only handles the administrative tasks of calculating wages and filing taxes while you remain the legal employer. For companies without a Dutch entity, an EOR is the superior choice because it eliminates permanent establishment risks and the need for local bank accounts or directors.

Frequently Asked Questions

You can hire employees in the Netherlands without incorporating a local entity by using an Employer of Record (EOR). The EOR acts as the legal employer, managing all payroll, tax, and social security obligations on your behalf. This allows foreign companies to enter the market quickly while remaining fully compliant with employment law Netherlands for foreign employers. It's the most efficient way to secure talent without the administrative burden of setting up a Dutch BV.

The mandatory holiday allowance is 8% of the employee's gross annual salary. This is a statutory requirement for all employees in the Netherlands and is typically paid as a lump sum in May. It's calculated based on the base salary plus any overtime or bonuses earned during the previous year. Employers must ensure this is clearly stated in the employment contract to avoid disputes during the annual payout period.

Beyond the gross salary, you should budget for employer social security contributions, which typically add 18% to 27% to the total employment cost. This percentage varies depending on the specific sector and the type of contract. You must also factor in the mandatory 8% holiday allowance and any secondary benefits such as pension contributions or travel allowances. These costs cover essential insurance for unemployment, disability, and healthcare foundations.

The 30% ruling is a tax incentive for highly skilled migrants that allows you to provide a 30% tax-free allowance on their gross salary. To apply, both the employer and employee must submit a joint application to the Dutch Tax Office (Belastingdienst) within four months of the start date. In 2026, the minimum taxable salary threshold is €48,013 for most professionals, or €36,497 for those under 30 with a qualifying Master's degree.

The maximum probationary period is two months for an indefinite contract and one month for fixed-term contracts longer than six months but shorter than two years. Contracts with a duration of six months or less cannot legally include a probationary period. During this window, either party can terminate the employment relationship immediately without providing a specific reason or observing a notice period. It's a critical phase for assessing the fit between the employee and the organization.

If an employee falls ill, you're legally required to pay at least 70% of their salary for up to 104 weeks. During the first year of illness, this payment must not fall below the statutory minimum wage. You must also follow the Gatekeeper Improvement Act, which mandates a strict reintegration process in partnership with an occupational health service (Arbodienst). Failure to document these reintegration efforts can lead to the UWV imposing a third year of mandatory wage payments.

Terminating a contract is more complex in the Netherlands because at-will employment doesn't exist. You generally need a valid legal ground and permission from either the UWV or a District Court, unless the employee agrees to a Settlement Agreement (VSO). Most employers choose the VSO route to avoid lengthy legal proceedings. This agreement allows both parties to part ways on mutually agreed terms, including the statutory transition payment and notice period.

An EOR acts as the legal employer of your staff, assuming all legal risks and compliance responsibilities under employment law Netherlands for foreign employers. A payroll provider only handles the administrative tasks of calculating wages and filing taxes while you remain the legal employer. For companies without a Dutch entity, an EOR is the superior choice because it eliminates permanent establishment risks and the need for local bank accounts or directors.